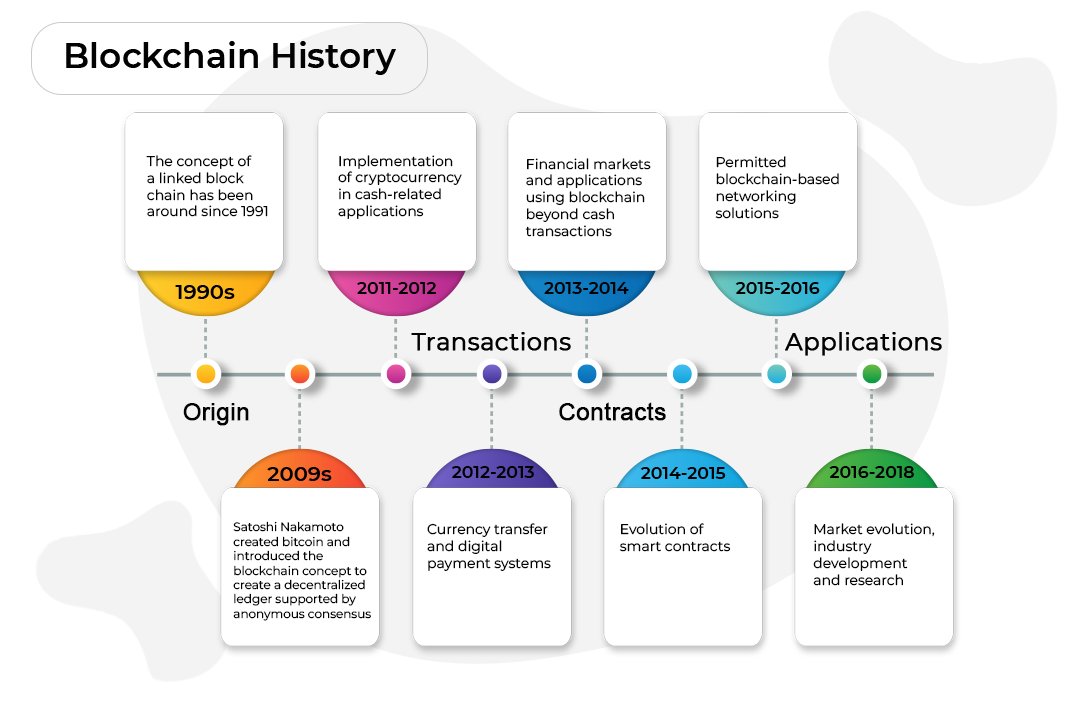

Blockchain history from 1991 to present day

Blockchain today means various cryptocurrencies, NFT tokens, crypto exchanges and wallets, as well as exchanges on which virtual assets are traded, and much more.

27.12.2021

4868

14 min

1

How did it all start? How did the cryptocurrency market take shape, and what opportunities do blockchain projects offer today? Let's get to the bottom of this in order.

How the technology began

Paper documents with a handwritten signature are easy to forge because all you need is the source, a ballpoint pen, and the will to do it. Electronic documents are stored centrally, in one large archive. Information is entered into the ledgers by people, which means it can be altered. Legal norms do not help. The only way out is to develop a technical solution.

In 1991, there was an idea to put time stamps on electronic documents so that they could not be issued retroactively or forged. After that, the documents were sorted by the same marks and collected in a single block. This is how the first prototype of the blockchain appeared.

The idea belongs to American cryptographers Stuart Haber and Scott Stornetta. In 1991, they presented their development, namely, a cryptographically secure blockchain. Thanks to it, no one could make changes to the timestamps of stored documents. A year later, the technology was refined to include Merkle trees, which made it possible to collect more documents in a single block.

Another technology that has contributed to the emergence of blockchain is a decentralized peer-to-peer network. In such a network, as a rule, there are no dedicated servers, and each node functions as both server and client.

A significant contribution to the development was made by Hashcash, the proof-of-work algorithm developed by Adam Back. It worked in the following way: each email user had a text stamp added to the email header, which indicated that the sender had spent some part of their time and resources to calculate this stamp. The algorithm made it much harder to conduct spam and DDoS attacks on mail servers.

And in 2008, the Internet changed forever: a person (or a group of people) under the pseudonym Satoshi Nakamoto sent out the White paper of a decentralized peer-to-peer electronic payment system, Bitcoin.

Satoshi Nakamoto is the man who started the blockchain. His real name is still unknown. In August 2021, Bloomberg published information confirming that Satoshi is Hal Finney.

“Giving a little more thought to the idea of buying and selling digital cash, I thought of a way to present it. We are buying and selling “cryptographic trading cards.” Fans of cryptography will love these fascinating examples of the cryptographic arts…”

Hal Finney

Bitcoin, the first blockchain-based cryptocurrency

Bitcoin as the first cryptocurrency was the starting point for an entire industry. The technology began to attract not only programmers and experienced investors but also ordinary people. The decentralized system, anonymity, and the ability to quickly send coins anywhere in the world played a significant role in the spread of bitcoin. Between 2015 and 2017, the average number of transactions grew from 100 000 to 300 000 per day. The novelty of the technology and the open code attracted not only high-tech fans but also ordinary people. This gradually led to problems with bandwidth, as the Bitcoin network could conduct 4 to 7 transactions per second, while Visa's payment system could conduct 24 000 transactions per second.

The bitcoin network was not ready for heavy loads, so it needed improvements, which are called forks. At the same time, it is important to distinguish between a source code fork and a blockchain fork. In the first case, we are talking about a new blockchain project with changed code, for example, the blockchain. The second one is about offering changes to all current members of the network.

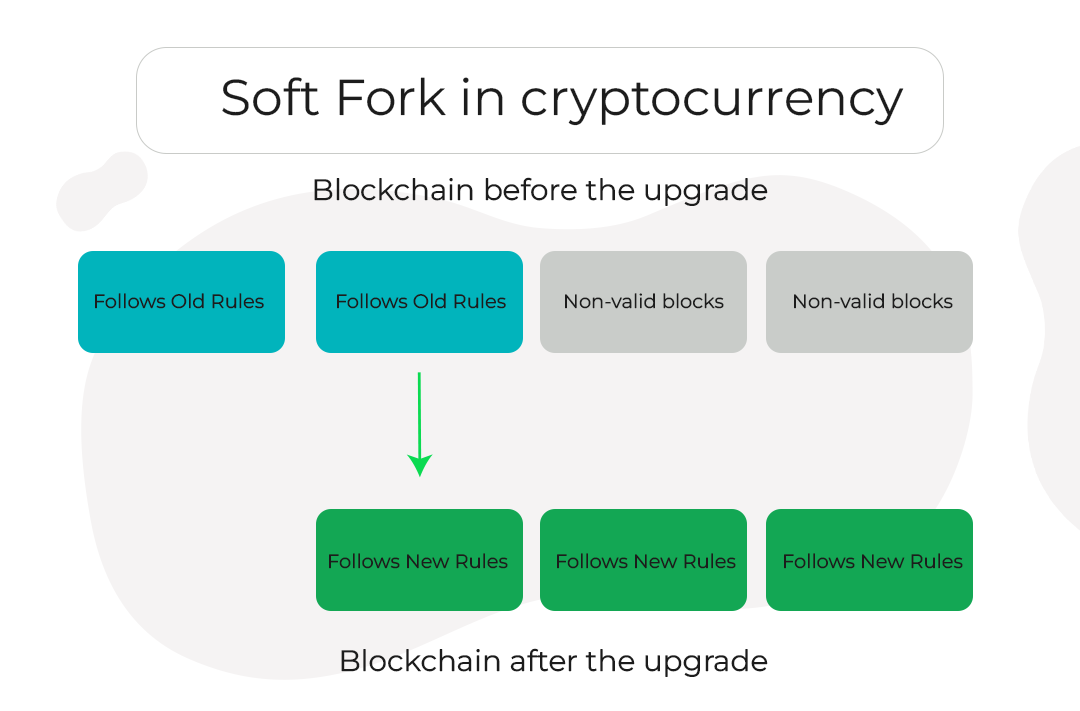

How do forks improve blockchain? Bitcoin is open-source software. Like any other software, it requires constant updates that fix problems and improve the level of performance. In the case of cryptocurrencies, these updates are called “forks.”

Two main types of fork: soft fork and hard fork

Soft fork. In the case of a soft fork, most of the participants (nodes) need to upgrade to the new version. At the same time, if some nodes do not accept the new rules, they can still interact with other nodes that have accepted them.

An example will illustrate this better. In one of the States of America, 100% of the people speak American English. A group of people come in and say: in order for everyone to be better off, we need to communicate in British English. Half of the people switch to British English, and the other half continue communicating in American English. Still, everyone understands each other.

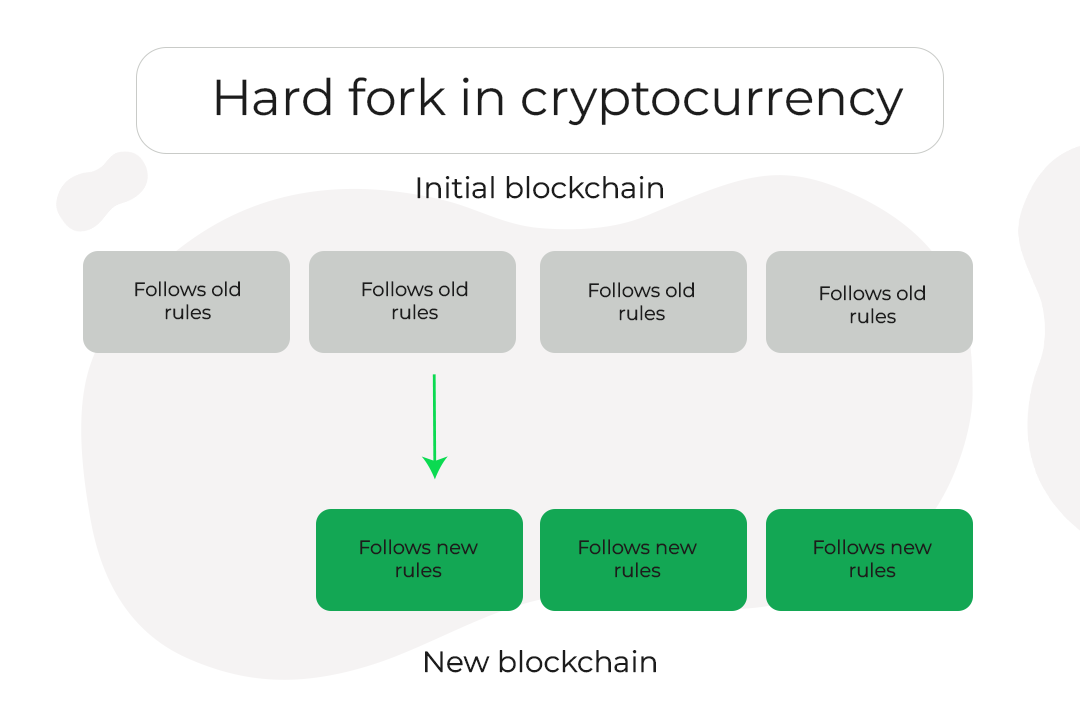

The hard fork is more serious. When you upgrade the client to a new version, the functionality changes so much that compatibility with older versions is lost. You get a new network in which the updated nodes do not notice the old ones. And then it all depends on the community:

- If most of the network users install the update, it switches to the new rules.

- If not, there appears a new network with a new coin, namely, altcoin.

Bitcoin XT

Two Bitcoin developers, Gavin Andresen and Mike Hearn started working on an alternative version of the bitcoin blockchain. The main idea was to increase the maximum block size from 1 MB to 8 MB, which would increase the network throughput to 24 transactions per second. The project was completed by August 2015. This is how the Bitcoin XT soft fork appeared.

In order to launch a fork of Bitcoin XT, the developers' changes needed to be supported by the majority of miners, 75% of the community, and there were problems with that.

The project was popular at first, but later the developers faced criticism from the community and major mining pools in China. The community saw the soft fork as a violation of the original bitcoin principles. As a result, the update was supported by less than 1%, and the project ceased to exist by 2016.

Bitcoin Classic

After the unsuccessful launch of Bitcoin XT, Gavin Andresen did not give up and continued his work. Together with another developer, Jeff Garzik, he started working on a new version of Bitcoin Core. The changes were not that radical: it was supposed to gradually increase the size of the block, at first, up to 2 MB, and after 2 years, up to 4 MB.

The soft fork was launched in January 2016 under the name Bitcoin Classic. The project was supported by major cryptocurrency exchanges and mining pools. But this fork also turned out to be unsuccessful. Bitcoin Classic began to lose popularity, and in November of the same year, a representative of the soft fork on the project's official website urged all users to switch to Bitcoin Cash.

Bitcoin Unlimited

In 2016, three developers Andrew Stone, Peter Tschipper, and Andrea Suisani offered another soft fork, Bitcoin Unlimited. And in this case, they did not communicate with the market in the language of ultimatums but came up with an offer. Users could independently choose block size by voting.

But Bitcoin Unlimited also failed. They found errors in the code, which opened up the possibility of a DDoS attack for scammers. This led to about 75% of the network's nodes failing due to memory leaks. That's the end of a significant bitcoin soft forks story and the beginning of another one, that is, hard forks.

Bitcoin Cash

Work on the first hard fork began in 2015. Blockchain developer Peter Wolle suggested another way: to abandon the idea of increasing the size of the block and to change the way transactions are stored. The update was supported by 95% of miners.

But a split began within the project. One of the development team leaders, a former Facebook engineer, raised the issue that the block size should be increased to 8 MB. This update also needed the consent of 95% of the community to launch, but the team decided not to take a vote and made an unplanned hard fork on their own. The big red button was pressed. On August 1, 2017, Bitcoin Cash appeared.

The update was supported by the current CEO of the Bitcoin.com magazine, Roger Ver, and the big ViaBTC mining pool.

The technical advantage of the fork was an increase in the maximum block size to 8 MB, which allowed the network to conduct 61 transactions per second. In addition, bitcoin and Bitcoin Cash operated on the same SHA-256 algorithm, which meant that miners could mine the coin that was profitable at that particular moment. In November 2018, due to Craig Wright's claims, Bitcoin Cash had another hard fork, and the chain split into two: Bitcoin ABC and Bitcoin SV.

Litecoin

While bitcoin has been called “digital gold,” Litecoin can be considered “digital silver.” Based on the bitcoin blockchain, Litecoin was not inherently designed as a replacement for bitcoin, but rather as a supplement.

The story of the project began with Charlie Lee. The task was simple, namely, to improve bitcoin, or rather, to create a convenient payment system and leave bitcoin as a means of preserving value. Any payment system must be fast. To this end, the developers reduced the time to form a block to 2,5 minutes and received a 4-fold gain in throughput.

The next step was a fork on GitHub: the developers copied the bitcoin code and made changes to it, after which they launched a separate network. The project was released on October 12, 2011.

The main purpose of Litecoin is digital payments for services and goods in stores. It is a kind of VISA analog, but relatively anonymous and decentralized.

Second-generation cryptocurrencies

The first generation of blockchain is Bitcoin. It works as a decentralized payment system with simple smart contracts, that is, conditions under which a transaction is performed. The problem is that they have extremely limited capabilities.

The second generation is Ethereum. It began with the launch of the network of the same name in 2015. For the first time, developers managed to implement the advanced functionality of smart contracts.

A smart contract is a standalone program designed to verify or execute a digital contract. In real life, smart contracts can be compared to a notary, who confirms the fact of the transaction.

Ethereum

In 2013, Vitalik Buterin, one of the founders of Bitcoin magazine, suggested a scripting language for creating decentralized applications.

A year later, in the second half of 2014, a crowdfunding campaign was launched to develop the project. The total amount was 31 591 bitcoins, the equivalent of $18,439,086 at the time. On July 30, 2015, the blockchain of Frontier alpha version was launched. Ethereum became a platform for creating decentralized services that are based on smart contracts.

There can be several contract terms, as well as transactions, which allow the development of separate applications, which are called DApps. And these are already platforms, exchanges, slot machines, and social networks. Now Ethereum is the first most popular altcoin. There are NFTs, thousands of DApps, and large decentralized platforms based on it.

TRON

Based on the functionality of smart contracts, entrepreneur Justin Sun launched a blockchain-based digital entertainment platform, TRON, in 2017. It is a network for the free exchange of content between users. They can upload, store and transfer content, rent it out, deploy a decentralized app, and issue their own tokens, to name just a shortlist of features.

EOS

Another project, EOS, run by lead developer Daniel Larimer, was completed in July 2017. This is a decentralized platform, which is ready to offer its user a high speed of transactions, but it is more tailored for highly loaded commercial purposes, for example, a large commodity business.

Third-generation cryptocurrencies

The new generation of any cryptocurrency begins with solving the big problems of the past. The third generation adds bridges between blockchains, that is, a connection between two blockchain ecosystems through which coins can be transferred, and which solves the problem of scalability.

In addition, third-generation projects rely on energy efficiency, increasingly abandoning PoW, and switching to PoS and other consensus algorithms. Also, the third-generation network allows the use of blockchain outside of payment systems.

Cardano

On September 29, 2017, the Cardano project, a platform for creating decentralized applications based on smart contracts, started working. The Cardano feature is the Ouroboros protocol, a consensus algorithm with provable cryptographic strength, which is the main reason why Cardano is considered a third-generation cryptocurrency. The main advantage is that it is the largest blockchain that already uses the Proof of Stake protocol.

Polka dot

In 2016, another generation project, Polkadot, was released, and this is one of the most complex projects in terms of architecture. The technical director of the project, Gavin Wood, was dissatisfied with the slow development of Ethereum and decided to create a project that would have everything that Ether could not.

The main idea of the technology is to connect different blockchains, for example, Ethereum and Bitcoin, combining them within a single blockchain. In addition, the technology solves the issue of the two-way compatibility of distributed ledgers.

Solana

Solana, led by Anatoly Yakovenko, was launched rather recently, in March 2020. While Ethereum is an alternative to Bitcoin, Solana is an alternative to Ethereum 2.0. The project is based on a blockchain running on Proof of History (PoH) and Proof of Stake (PoS) protocols. The first protocol allows you to record a transaction before the information is added to the blockchain, thereby increasing throughput. The second one allows users to earn coins for staking.

Other popular cryptocurrencies

In the world of cryptocurrencies, there are many projects that do not fit into the general classification but have already become popular. Let's talk about the most famous ones.

Ripple. The project was released in 2012. Ripple is a protocol, a currency exchange, and a money transfer system. The main idea of the project is openness and cooperation with state structures. The main clients are banks that use xCurrent software. It can be used to track cross-border transfers in real time.

NEM. The official launch was on March 31, 2015. The cryptocurrency received its market share due to the lack of emission, that is, there are only 9 billion coins in circulation. The peculiarity of NEM is that its blockchain uses a proof-of-value algorithm. It considers three account characteristics:

- wallet balance;

- the number of transactions made by the account;

- the time the account has been online.

NEM also integrates an encrypted messaging system and the Eigentrust++ reputation system.

Tether. A token whose value is backed by reserves of US dollars. It is a low-volatility digital asset, the rate of which is rigidly tied to the dollar exchange rate. Tether became the ancestor of stablecoins, the link that connects the cryptocurrency market with real-world assets.

Waves. A platform that can be used to issue tokens for startups' crowdfunding campaigns. It was created by entrepreneur Alexander Ivanov in 2016, inspired by the NXT cryptocurrency. His team included developers who were previously involved in the development of this project. Today, the work on Waves Enterprise is still in progress.

Dogecoin. A meme coin, which is often mentioned by the head of Tesla, Elon Musk. The story of its origin is quite ironic. Developer Jax Palmer decided to make a joke and created his own cryptocurrency to show the world that investing huge money in an unstable direction of cryptocurrencies is absurd. But Elon Musk's constant pump proved otherwise.

Another purpose of creating this project is to show that the anonymity of cryptocurrency can be used not to sell drugs, but, for example, to direct it to charity.

Anonymous Cryptocurrencies

Most cryptocurrencies do not require personal information to use and make transactions, which is why they have gained a reputation for anonymity. But is this really the case? What does it take to track a transaction?

A simple desire is enough because blockchain is an open database, which means that anyone can see the list of transactions, starting with the very first one. To prevent this, anonymous cryptocurrencies were created.

Dash was launched in January 2014. The project is focused on increased transaction speed and anonymity through the PrivateSend mixing mechanism. The high speed of transactions without additional fees is provided by the InstantSend technology.

Monero. Another cryptocurrency for anonymous transactions appeared in 2014. Anonymity is provided by stealth addresses and circular transaction signatures. In this network, only the participants of the transaction, as well as those to whom the access key is provided, know the amount, the address of the sender and the recipient.

Zcash. The Zerocash project was launched in 2016. Anonymity is ensured by zk-SNARK technology based on the zero-disclosure proof principle. This allows verification of the mathematical validity of the transaction but does not provide information about the second exchanger.

Why will the history of blockchain never end?

The first attempts to create a distributed registry began back in 1991. But the rules of the game changed seriously when Satoshi Nakamoto developed blockchain-based cryptocurrency in 2009. The technology began to evolve: more than 13 000 altcoins, three generations of blockchain, decentralized platforms that solve problems for business, government, and each of us. And this is far from being over.

New protocols are emerging, problems are being solved, and algorithms are being improved. Only one fundamental solution, invented 12 years ago, remains unchanged.

Useful material?

Telegram

Telegram  Twitter

Twitter Basics

Why Satoshi Nakamoto’s technical manifesto for a decentralized money system matters

Oct 31, 2022

Basics

Experts evaluated the development prospects of the new ecosystem and the investment attractiveness of its token

Oct 20, 2022

Basics

How to track fluctuations correctly and create an effective income strategy

Sep 13, 2022

Basics

Review of the most profitable offers from proven trading platforms

Aug 29, 2022

Basics

The Ethereum Foundation team has published a breakdown of major misconceptions about the upcoming network upgrade

Aug 18, 2022

Basics

What benefits the exchange offers, and what else is in the near future

Aug 4, 2022

Cryptocurrency rates

-

Bitcoin

$62 975

BTC

-0.71%

-

Ethereum

$2 551.16

ETH

+3.56%

-

BNB Smart Chain

$579.4

BSC

+1.23%

-

Ripple

$1.07

XRP

-0.58%

-

TRON

$0.160134

TRX

-1.59%

-

Dogecoin

$0.069919

DOGE

-0.09%

-

Zcash

$476.66

ZEC

+0.61%

-

Cardano

$0.18547

ADA

+3.18%

-

Stellar XLM

$0.171515

XLM

-1.28%

-

Polkadot

$3.32

DOT

+5.27%