The inner workings of Celsius. What led to the collapse of one of the largest cryptocurrency lenders

How the pursuit of quick profits and fraudulent schemes turned into bankruptcy

22.07.2022

2517

7 min

0

On June 13, crypto lending platform Celsius suspended withdrawals and transfers due to tough market conditions, and a month later filed for bankruptcy. In the community, the situation has been called crypto’s “Lehman Brothers moment,” named after the investment firm that just as unexpectedly collapsed in 2008, triggering the global crisis. As in the case of Celsius, many factors led to it, including the situation inside the company. Let's find out what was going on behind the scenes at Celsius and how Sam Bankman-Fried, head of the FTX exchange, was involved.

Celsius' bankruptcy

The first alarms for the platform began before the global crypto winter, when rising interest rates prompted investors to liquidate potentially risky assets. As early as May, when the Terra ecosystem collapsed, the Celsius economy finally crashed. At its core, the platform relied only on money from retail investors, which it subsequently lent to other cryptocurrency companies and used for ill-considered investments.

At the first bankruptcy hearing, Celsius' lawyers said that most of the client funds on the platform were at the full disposal of the company. Attorneys cited the company's terms and conditions, which state that 77% of the assets were pledged under an “earnings program.” That means that, according to the platform's rules, Celsius can use them however it wants.

The company accumulated about $20 billion in deposit accounts. This is not surprising, since the platform offered interest rates of up to 18% per annum on cryptocurrency deposits. The head of the company, Alex Mashinsky, has always personally stated that Celsius' investment schemes are sound and reliable. “We are actually safer than most banks,” he said in an interview in 2020.

Before filing for bankruptcy, the company managed to pay off its creditors represented by DeFi-Protocols Maker, Aave, and Compound. In total, Celsius recovered $1 billion in collateral. The filing itself involves a financial restructuring. Celsius said it had $167 million left in its accounts, which would be used to maintain liquidity.

At this point, the scandals surrounding the lending protocol were not about to subside. In early July, Jason Stone, one of Celsius' former asset managers, sued the company. According to the accusation, Celsius used its clients' funds uncontrollably in risky trading strategies, resulting in the loss of a huge amount of money. In the lawsuit, Stone also pointed to the platform's inability to make payments to investors and noted “severe exchange rate losses.”

Semi-legal schemes and shadow documentation

Financial Times reporters examined Celsius' documents and reports and found many inconsistencies. Even the company's supervisory department pointed to flaws in internal accounting systems and misrepresentation of financial statements. Also, documents requested by the US Securities and Exchange Commission (SEC) said that several Celsius co-founders, including Daniel Leon, sold personal stocks of the CEL platform's native token directly to the company several times.

This is just one of the strange token manipulations seen at Celsius. A particular component of the company's business model was that it only offered the highest rates to customers who agreed to receive payments in CEL token. Given that Celsius owned most of its own asset, it essentially had complete control over the price of the token. Prior to the funds freeze, the company bought back a certain percentage of CEL on a weekly basis to maintain its balance. According to Arkham Intelligence, Celsius has spent $350 million buying its own token since July 2019.

Managers took advantage of CEL's rising price for their own purposes. On the same day that Leon published a video in which he talked about the cryptocurrency's bright future, Celsius transaction records list the sale of Leon's personal CEL tokens to the company for $1,8 million. Sixteen such transactions were found to have taken place between October 2020 and August 2021. According to the documents, the total amount of such transactions is estimated at $11,4 million. Other Celsius managers sold $40 million worth of CEL tokens during the same period.

CEO Alex Mashinsky made only one such transaction for $500 000. Some employees interviewed, however, believe he may have made transactions through other accounts and addresses. Based on blockchain records, Arkham analysts estimated that Mashinsky sold $44 million worth of CEL through exchanges.

According to internal documents, the company began investing in DeFi-services in 2020 without proper diligence on projects or proper systems to track assets. Last February, the internal oversight department sent a warning that some employees may have invested money in new funds without explicit permission or compliance checks. The document also said brokers could move assets from one fund to another unnoticed by management, allowing them to hide losses and the real value of assets under management.

How Celsius lost its customers' hundreds of millions of dollars on high-risk schemes

According to former employees, tracking Celsius' assets was difficult. Sometimes internal databases produced different AUM (assets under management) values, and the company's reconciliation process, called “the freeze,” often resulted in inconsistencies.

Even before the bankruptcy, the cryptocurrency exchange FTX refused its deal with Celsius. The terms implied buying the platform, or giving it financial support to solve its liquidity problems. Studying the company's financial data, FTX experts found a balance sheet discrepancy of $2 billion, which was the reason for the rejection.

What does Sam Bankman-Fried have to do with it?

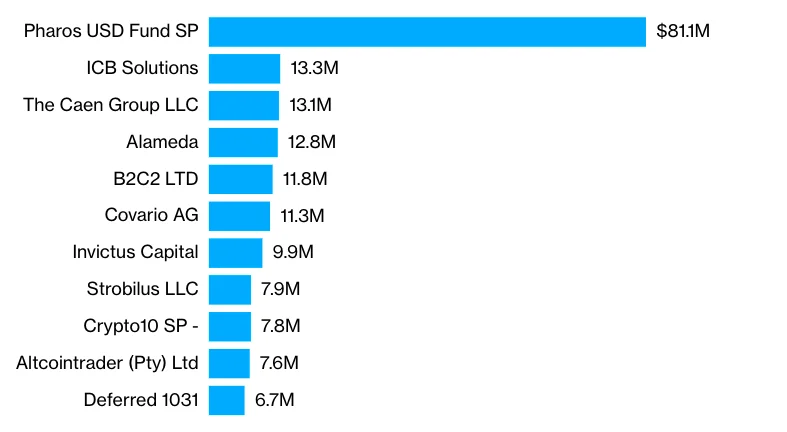

After Celsius filed for bankruptcy, more details about its finances emerged. According to documents, the company has more than 100 000 creditors, among which Pharos USD Fund SP stands out, to which Celsius owes $81 million. That's almost six times more than the second-largest creditor.

Celsius' creditorsSource: Bloomberg.com

A simple Google search of the company's name gives no results. However, according to a Bloomberg investigation, the website of technology firm Lantern Ventures describes it as a “London-based proprietary trading firm focused on cryptocurrencies.” In fact, Pharos USD Fund SP is one of Lantern's affiliates. According to documents filed with the SEC, it has about $400 million under management, more than half of which is held by investors outside the United States.

Digging deeper, we find that many Lantern employees have careers that in one way or another intersect with Sam Bankman-Fried, the head of the FTX exchange. Lantern CEO Tara Mac Aulay, for example, co-founded Alameda Research, a company owned by Bankman-Fried, which is also on the list of Celsius creditors. The platform owes her $12,8 million. As of May 2021, Mac Aulay is listed as Lantern's largest shareholder.

Three other employees, according to their bios on LinkedIn, worked for either the charity Giving What We Can or its affiliate, of which Bankman-Fried is also listed as a member. Another employee, Victor Xu, was a head trader at Alameda for nine months in 2018.

Perhaps even before the cancelled deal, the head of FTX was indirectly affiliated with Celsius. It' not surprising, as Bankman-Fried has become one of the central characters in the recent cryptocurrency market shakeup. Previously, Alameda provided a $250 million loan to BlockFi, as well as two loans to cryptocurrency broker Voyager Digital to support liquidity.

Taken together, Celsius' collapse happened because of inept financial management and the downturn in the crypto market. It is likely that some internal details will remain undisclosed, but we can already say that the main business model of the lending protocol was built on shadow returns from risky investments.

Useful material?

Telegram

Telegram  Twitter

Twitter Research

One and the same cryptocurrency address received two completely opposite assessments from different analytics systems: from an ordinary gambling service to an extremely severe criminal offense. This story has become the starting point for a broader conversation about what the scientific standards of blockchain analysis should look like — and why errors in systems like these can shape the fates of real people.

Jul 1, 2026

Research

The blockchain has helped uncover the ties between cryptocurrency fundraising campaigns, exchangers in Syria, and intermediaries in several countries around the world. A telltale pattern has emerged in which the same addresses were used across multiple donation drives at once

Jun 24, 2026

Research

Four Iranian cryptocurrency exchanges accounted for roughly 78% of all digital asset volume tied to the country in 2025. They have now become the focal point of the largest U.S. sanctions campaign against Iran's cryptocurrency infrastructure.

Jun 5, 2026

Research

A financial system is already up and running on public blockchains, with loans, analogues of U.S. Treasuries, and automated capital markets. More than $551 billion has flowed through DeFi protocols — but most of that activity has nothing to do with the real economy and everything to do with the speculative build-up of risk.

May 29, 2026

Research

Around 97% of Chinese suppliers of chemicals used to make fentanyl accept payment in cryptocurrency. The volume of such transactions continues to grow alongside the global market for synthetic drugs

May 22, 2026

Research

For the first time, the new law makes blockchain analytics an officially mandatory tool of financial oversight in the United States. Authorities will also gain the power to restrict transactions with foreign crypto services tied to money-laundering risks.

May 20, 2026

Cryptocurrency rates

-

Bitcoin

$62 672

BTC

-0.63%

-

Ethereum

$2 551.16

ETH

+3.56%

-

BNB Smart Chain

$579.4

BSC

+1.23%

-

Ripple

$1.07

XRP

-0.98%

-

TRON

$0.160134

TRX

-1.59%

-

Dogecoin

$0.069394

DOGE

-0.72%

-

Zcash

$478.97

ZEC

+1.16%

-

Cardano

$0.186416

ADA

-0.46%

-

Stellar XLM

$0.171165

XLM

-2.05%

-

Polkadot

$3.32

DOT

+5.27%