What is CBDC currency in simple terms: how central bank digital currency works

In this article, we explain in simple terms why CBDCs are being created, how they work, and how they differ from cryptocurrencies, stablecoins, and electronic money.

06.11.2025

832

15 min

0

In recent years, we have increasingly heard the acronym CBDC — central bank digital currency — being discussed by economists, governments, and users around the world.

But what does this term actually mean? Why is such a currency needed, and how does it differ from familiar electronic transfers or cryptocurrencies such as bitcoin?

In this article, we will explain what CBDC is in simple terms, how the system works, which countries are already testing or implementing their digital currencies, and what this could mean for each of us.

Content:

- What is CBDC in simple terms?

- How CBDC differs from cryptocurrencies, stablecoins, and electronic money

- Why do we need CBDC digital money?

- How CBDC works

- Issuance and control

- Where is CBDC digital money stored and how can it be used?

- Do CBDCs use blockchain?

- Public or private systems

- Why are countries introducing CBDCs

- Types of CBDC

- Examples and CBDC projects around the world

- China (e-CNY)

- European Union (e-Euro).

- Russia (digital ruble)

- Nigeria (eNaira)

- Brazil (Drex)

- India (e-Rupee)

- United States (Digital Dollar)

- The role of international organizations

- How are countries implementing CBDCs?

- Advantages and risks of CBDCs

- The future of CBDC: utopia or inevitability?

- Prospects for CBDC development

What is CBDC in simple terms?

CBDC is a central bank currency in digital form.

It is not a private initiative or a cryptocurrency, but an official means of payment issued by a country’s central bank.

Each digital unit of CBDC is equivalent to regular money: one digital dollar, euro, or ruble has the same value as its physical counterpart.

How CBDC differs from cryptocurrencies, stablecoins, and electronic money

CBDCs perform the same functions as traditional currencies, but in a digital format. They can be used for payments, savings, and investments. They help reduce the share of cash transactions and simplify transaction tracking.

Unlike decentralized cryptocurrencies, CBDCs are issued and regulated by central banks, which ensures stability and trust.

CBDCs combine the advantages of digital currencies with the reliability of traditional financial systems. They are not subject to sharp exchange rate fluctuations, as they are fully backed by the national currency at a 1:1 ratio.

| Parameter | CBDC | Cryptocurrencies | Stablecoins | Electronic money |

| Issuer | Central bank | Community (decentralization) | Private companies | Financial institutions |

| Regulation | Fully regulated | None | Partial | Under supervision |

| Collateral | Government assets | None | Fiat reserves | Customer funds |

| Legal status | Legal tender | No official status | Private asset | Financial instrument |

It is incorrect to say that CBDCs are cryptocurrencies. They remain part of the fiat system and are based on trust in the state and its central bank.

Simply put, this means that CBDCs are backed by governments, which is not the case with cryptocurrency projects.

While bitcoin aims to create a new financial system from the outside, the emergence and growing popularity of cryptocurrencies have stimulated significant innovation within the traditional finance sector itself, based on the idea of virtual currency.

According to the Bank for International Settlements, by early 2019, most of the world’s central banks were already engaged in research into the development of virtual currencies.

Why do we need CBDC digital money?

CBDCs are created as a modern alternative to cash and traditional bank transfers. They simplify payments, make them faster and safer, and open up financial services to more people.

The main goals of introducing CBDCs:

- Reducing transaction costs and increasing payment speed.

- Combating the shadow economy and increasing the transparency of financial transactions.

- Financial accessibility — the ability to receive payments even without a bank account.

How CBDC works

Central bank digital currency functions similarly to physical money and can be used for transactions such as paying employees or purchasing goods and services. Many countries are currently developing their own CBDCs, which may have different characteristics and functions, but all follow a common concept.

Issuance and control

CBDC issuance is carried out exclusively by the central bank. It determines:

- the total amount of issuance,

- the principles of circulation,

- the mechanism of regulation and reporting.

These decisions are made at the state level, which makes the system stable and reliable.

Where is CBDC digital money stored and how can it be used?

Users will be able to store CBDC digital money:

- in official wallets linked to the central bank;

- through commercial banks acting as intermediaries.

It is as easy to use as paying via a mobile app: instant transfers, online purchases, and government payments.

Do CBDCs use blockchain?

Some CBDCs are built on blockchain, but unlike cryptocurrencies, they use permissioned (private) networks. Only banks and regulators have access to them. Other projects are based on centralized databases that provide control and confidentiality.

Public or private systems

Blockchain and distributed ledger technology (DLT) are at the heart of CBDCs.

Blockchain is a decentralized ledger that records transactions securely and transparently.

DLT is a distributed ledger that allows multiple parties to have simultaneous access to the same data.

CBDCs can operate on a centralized or decentralized blockchain. In a centralized blockchain, the central bank has complete control over the network and can modify the ledger as needed. In a decentralized blockchain, the network is maintained by a group of validators who reach consensus on the state of the ledger.

DLT and blockchain have advantages over traditional payment systems: they are faster, cheaper, and more secure. They also provide greater transparency and accountability, as transactions are recorded in a public ledger.

- Public (example: Sand Dollar, Bahamas) — operate on an open DLT protocol.

- Closed (example: e-CNY, China) — operate in centralized ecosystems under the control of the central bank.

Why are countries introducing CBDCs

The introduction of CBDCs is not just a technological trend, but a strategic move that could change a country’s entire financial system. Countries see a number of advantages in central bank digital currencies that could make their economies more transparent, sustainable, and modern.

- Combating the shadow economy. CBDCs help track financial flows, preventing tax evasion and money laundering.

- Competition with cryptocurrencies. Countries are creating cryptocurrency-like instruments to offer citizens a legal alternative to private tokens.

- A macroeconomic policy tool. CBDCs allow governments to respond more quickly to crises — for example, by transferring funds directly to citizens.

- Financial inclusion and cost reduction. The CBDC system makes financial services available in regions without banking infrastructure.

Types of CBDC

There are two main categories of central bank digital currencies (CBDCs):

- The first is wholesale, intended for financial institutions and used for interbank payments or securities settlements.

- The second is retail, available to the general public. It expands access to central bank digital money for citizens.

Later, a third category appeared — two-tier. In such a system, CBDC is distributed through intermediaries, and the structure of requirements is similar to the existing financial system.

| Type | For whom | Application | Example |

| Retail | For the public | Payments, transfers, government services | e-CNY (China) |

| Wholesale | For banks | Interbank settlements | Project Helvetia (Switzerland) |

| Two-tier (Hybrid) | Through intermediaries | Balance between security and scale | e-RUB (Russia), e-EUR (EU) |

Examples and CBDC projects around the world

According to the Atlantic Council CBDC Tracker, more than 130 countries are exploring the introduction of CBDCs. Of these, more than 20 have moved on to active pilots or launched full-fledged systems.

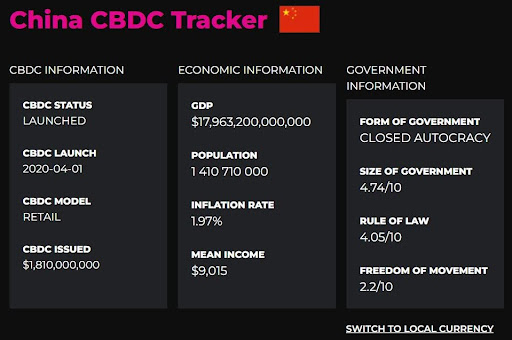

China (e-CNY)

China’s digital currency electronic payment (DCEP) system has been in development since 2014. However, the digital yuan is not a blockchain project based on a decentralized ledger. It uses a centralized database that records and tracks all transactions and controls access to them. The electronic yuan is backed by physical yuan at a 1:1 ratio.

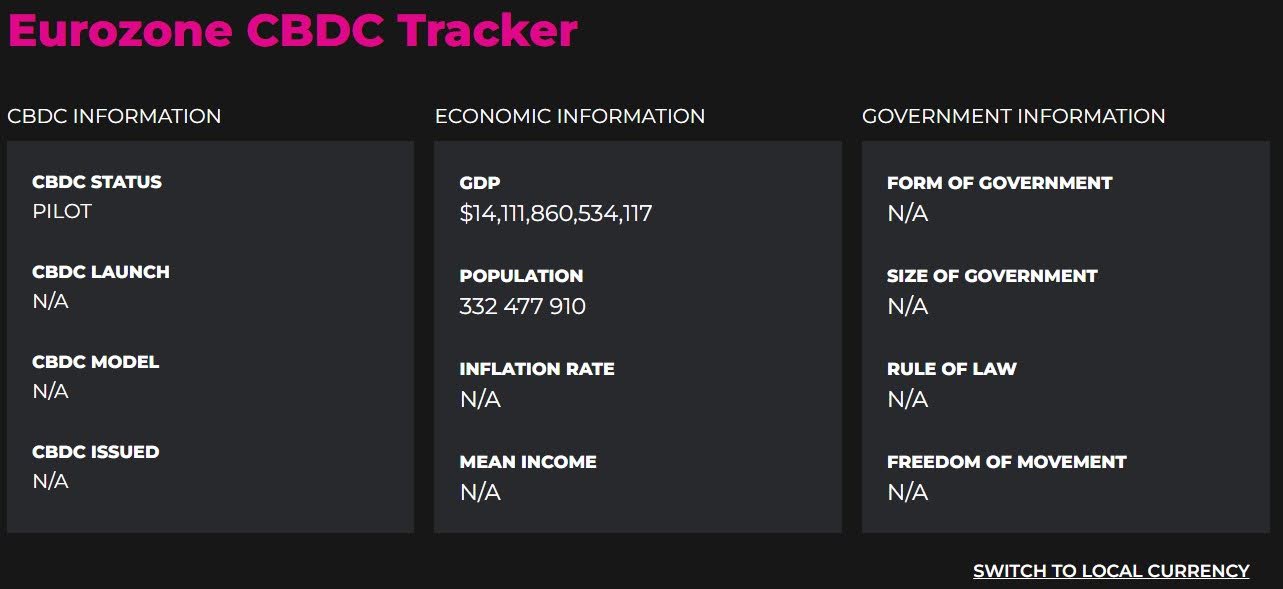

European Union (e-Euro)

The CBDC project is currently in the testing phase, with launch expected after 2026. The European Central Bank (ECB) signed agreements with seven technology companies to develop the infrastructure. The e-Euro is expected to launch by 2029, subject to legislative approval.

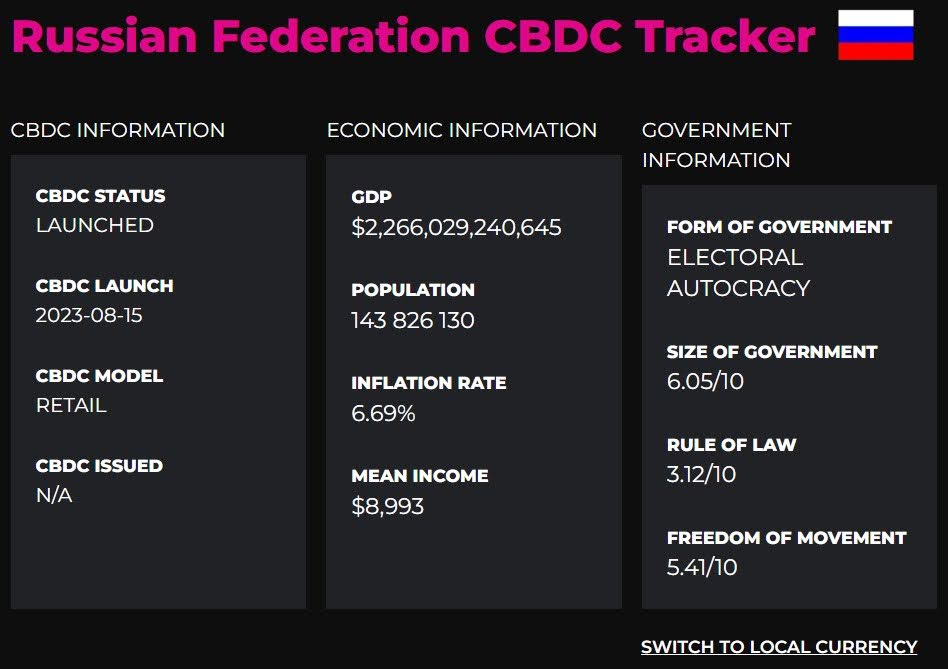

Russia (digital ruble)

In October 2020, the Bank of Russia published a consultation paper on the possibility of issuing a digital ruble. In June 2021, the regulator created a pilot group of 12 banks to test the CBDC. In July 2025, the Russian government approved a law requiring all banks to switch to using the digital ruble by September 2028.

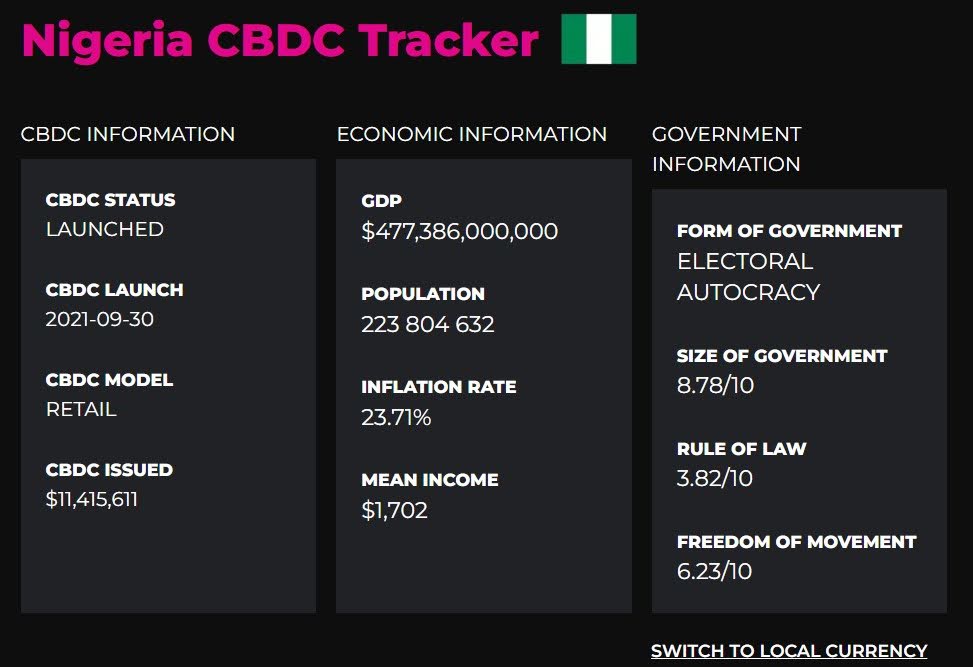

Nigeria (eNaira)

The e-Naira is Africa’s first digital currency, launched by the Central Bank of Nigeria in October 2021. After its launch, the e-Naira faced technical problems, public skepticism, and competition from other digital payment platforms. In February 2025, the Central Bank of Nigeria reported that the volume of e-Naira in circulation had grown to 18,31 billion naira ($11,4 million), representing 0,37% of the total currency in circulation.

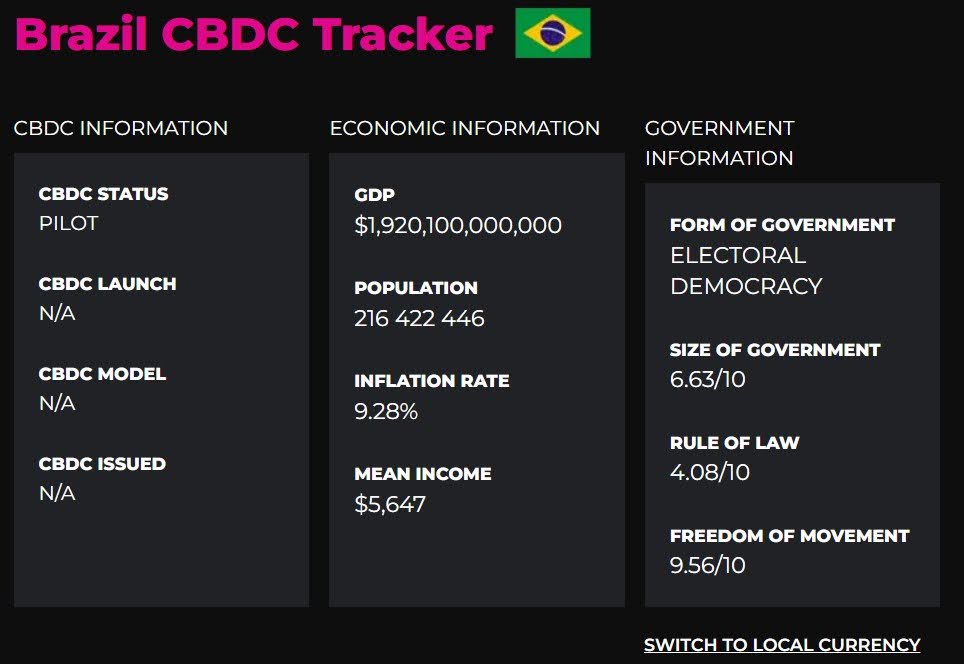

Brazil (Drex)

In August 2020, the Central Bank of Brazil established a working group to discuss the issuance of digital currency in Brazil. Drex provides for the functions of programmable money, tokenization, and conditional payments. During the pilot stages, difficulties arose with confidentiality and technical implementation. In June 2025, Brazilian Central Bank representative Rogério Antônio Lucca announced that the third phase of the Drex pilot project would focus on tokenization, consumer lending, and transaction efficiency.

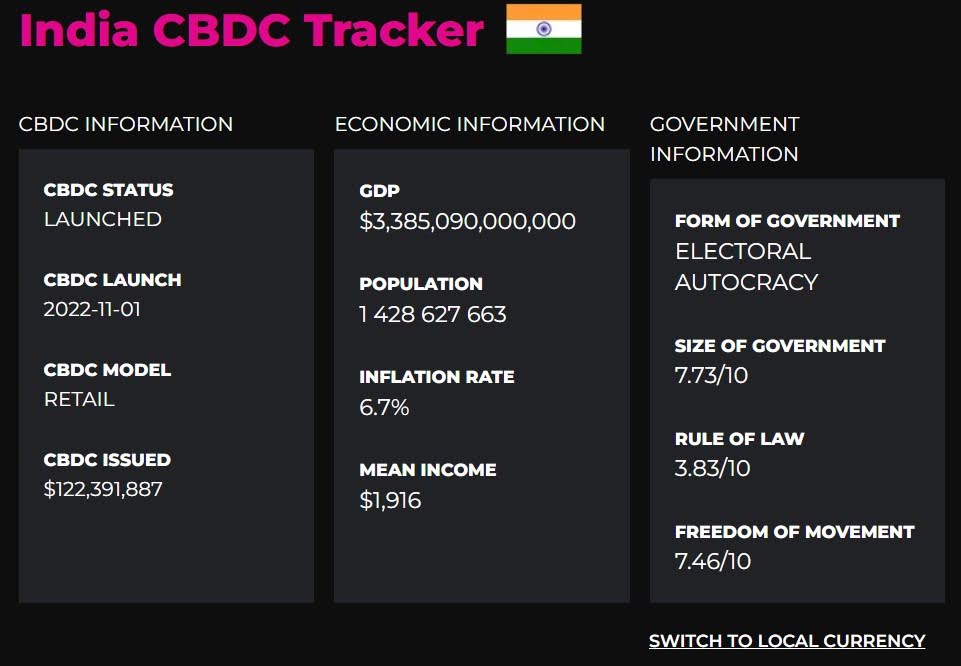

India (e-Rupee)

The idea of a digital rupee was first discussed in 2017, with a pilot launch taking place at the end of 2022. In May 2025, the Reserve Bank of India reported that e-Rupee turnover had grown from 2,34 billion rupees ($27 million) to 10,15 billion rupees ($120 million). Seventeen banks and 6 million users are participating in the project, including 88 000 women who have received social benefits through CBDC.

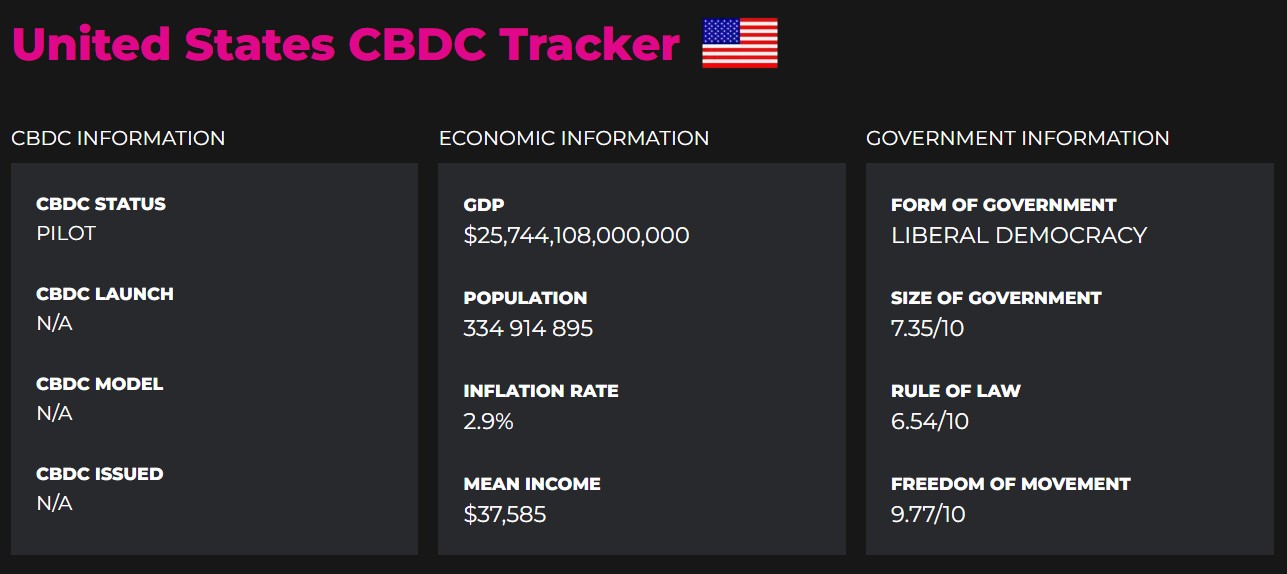

United States (Digital Dollar)

The United States has not yet implemented the digital dollar. The Federal Reserve has released a number of documents describing the possible format of CBDC. By the end of 2025, it plans to complete the research stage and publish technical specifications. In 2026–2027, testing will be conducted with the participation of businesses and citizens. If the results are successful, the digital dollar could be launched in 2028.

The role of international organizations

The Bank for International Settlements (BIS) helps develop compatibility standards between CBDCs from different central banks.

The International Monetary Fund (IMF) advises countries on cybersecurity and economic risks.

The World Bank supports infrastructure and technology initiatives.

How are countries implementing CBDCs?

Implementation is taking place in stages:

- Research and modeling

- Pilot testing with a limited number of participants

- Regulatory adjustment and risk assessment

- Full launch of CBDC at the national level

Banks, IT companies, regulators, and fintech partners are involved in the process.

Advantages and risks of CBDC

In recent years, central bank digital currencies have been seen as a possible solution to problems associated with the growth of cashless payments and the emergence of private cryptocurrencies.

- Improved payment efficiency. CBDCs speed up and reduce the cost of transactions, as they allow money to be transferred instantly and securely without intermediaries.

- Promoting financial accessibility. CBDCs provide access to financial services for people who do not use bank accounts or have limited access to them.

- Improving monetary police. CBDCs expand the tools available to central banks for managing the money supply and controlling inflation. The ability to set a fixed supply helps maintain price stability.

Potential benefits come with risks and challenges. This section will look at some of the main risks and challenges associated with the introduction of CBDCs:

- Security and privacy. Digital currencies are vulnerable to cyberattacks and hacking. Central banks need to implement robust data and system security measures.

- Risk of financial disintermediation. CBDCs could reduce demand for bank deposits, weakening the role of commercial banks and changing the structure of the financial system.

- Impact on traditional banking systems. The growth of CBDC use could reduce the popularity of credit cards and bank transfers, affecting the revenues of financial institutions.

| Pros | Cons |

| For the state | |

| Increased effectiveness of monetary policy | Risk of destabilizing the banking system |

| Strengthening sovereignty over the monetary system | Technological risks and implementation costs |

| For users | |

| Ease of use | Loss of privacy |

| Lower fees | Cyber threats |

The future of CBDC: utopia or inevitability?

Several development scenarios are possible in the future:

- Gradual replacement of cash and bank cards.

- Transition to cross-border settlements between CBDCs of different central banks.

- Creation of international platforms for digital currency exchange.

Successful cases

China and India have shown that central bank digital currencies (CBDCs) can be used by millions of people. In China, success was ensured by government support and extensive testing in major cities. In India, the spread was facilitated by the integration of CBDCs with local businesses and financial institutions.

Failed cases

In Nigeria, the slow adoption of e-Naira is due to its phased implementation and low public awareness. A year after its launch, 98,5% of e-Naira wallets remained inactive, despite the technical stability of the system.

In Jamaica, the development of CBDC was hampered by low user awareness, difficulties in connecting merchants, and problems with updating their payment terminals.

Global implications

CBDCs have the potential to change the structure of the global financial system, reduce the role of SWIFT, and strengthen the position of countries ready for the digital transition. International digital currencies issued by central banks could become the new standard for global settlements.

Prospects for CBDC development

Central bank digital currencies (CBDCs) are an important step in the evolution of the global financial system. They open up new opportunities for improving payment efficiency, financial transaction transparency, and access to banking services.

At the same time, the introduction of CBDCs requires a cautious approach: it is necessary to take into account the risks associated with cybersecurity, data privacy, and the impact on commercial banks.

The main task for governments and financial institutions is to find a balance between innovation and stability, ensure public confidence in the new form of money, and create a legal framework for the safe use of digital currencies. If implemented correctly, CBDCs could become a key tool for modernizing financial infrastructure and strengthening the economic sovereignty of states.

Useful material?

Telegram

Telegram  Twitter

Twitter Basics

Why Satoshi Nakamoto’s technical manifesto for a decentralized money system matters

Oct 31, 2022

Basics

Experts evaluated the development prospects of the new ecosystem and the investment attractiveness of its token

Oct 20, 2022

Basics

How to track fluctuations correctly and create an effective income strategy

Sep 13, 2022

Basics

Review of the most profitable offers from proven trading platforms

Aug 29, 2022

Basics

The Ethereum Foundation team has published a breakdown of major misconceptions about the upcoming network upgrade

Aug 18, 2022

Basics

What benefits the exchange offers, and what else is in the near future

Aug 4, 2022

Cryptocurrency rates

-

Bitcoin

$64 244

BTC

-0.5%

-

Ethereum

$2 551.16

ETH

+3.56%

-

BNB Smart Chain

$579.4

BSC

+1.23%

-

Ripple

$1.03

XRP

-2.5%

-

TRON

$0.160134

TRX

-1.59%

-

Dogecoin

$0.068976

DOGE

-1.5%

-

Zcash

$497.11

ZEC

-4.2%

-

Cardano

$0.200606

ADA

+5.6%

-

Stellar XLM

$0.161084

XLM

-2.7%

-

Polkadot

$3.32

DOT

+5.27%